products & services

Travel sector to see recovery through buy now, pay later

Easing lockdown restrictions across the globe carries some hope in allowing foreign travel to certain parts of the world. The only difference now is that depending on the traffic light system in the UK, it’s likely that a vacation comes with multiple Covid-19 tests and quarantining, so with larger families, this quickly becomes unaffordable. Jaimini Pattani writes

B

uy Now, Pay Later (BNPL) can kick off tourism while making holidays and travel more affordable for consumers; at the same time, as soon as the green list starts to expand, there will be a rapid surge in holidaymakers. However, a percentage of these are in the furlough or redundancy category, making even low-cost holidays difficult to obtain.

We have all heard of the BNPL boom for lifestyle purchases such as clothing and furniture during the pandemic through the likes of Klarna and Zilch, but what is now becoming more apparent post-lockdown is that the tourism industry is stagnant and will take time to recover, years even.

Two firms in the UK that have followed Klarna and Expedia’s 2019 travel now, pay later partnership are Fly Now, Pay Later and Butter, which offer customers the chance to split flight and hotel costs into instalments.

When we look at the latest data on the GlobalData UK Sentiment Tracker, consumers look to save more over the next six months (compared to the pre-pandemic levels in early 2020). Therefore, the opportunity to travel using BNPL options permits consumers to maximise their savings and salary for that period.

In addition to this, research carried out by Butter found that 78% of holidaymakers have said that spreading the cost would influence their probability of booking a holiday this year.

BNPL – a threat to credit cards?

BNPL for goods in-store and online was the initial threat to credit cards. It’s our view that spreading the cost of travel will surge in popularity too, which suggests that using credit cards for vacations could be less frequent.

Banks will now certainly have to include some sort of BNPL option into their strategies, as it’s becoming apparent that the list of goods and services under instalment options is expanding. BNPL has broken down barriers and has aimed to close the gap between consumers and mainstream lending by providing alternate options to consumers, while expanding their presence in ecommerce and the digital wallets space.

American Express has started offering US customers the option to pay for flights through BNPL instalment options, which suggests that the credit card space could be catching up to BNPL rivals.

Generally, though, banks and other lenders are still far away from offering anything similar, and in our view are not likely to do so anytime soon. Moreover, with the market being inundated with alternate lending, payment options, and new credit-scoring methods, mainstream lending is becoming less attractive to consumers, especially those in the younger cohort.

The launch of BNPL travel options will likely appeal to a generation above this, thus making more consumers accepting of BNPL as time goes on. This acceptance will only strengthen when the service becomes appealing to a broader demographic, and in our view, this is happening now in the market.

Acceptance occurs once the service starts to serve the needs of consumers, and this is exactly what travel instalment payment options are aiming to achieve.

Overall, the downside to customers will be the lack of protection offered through BNPL, as using BNPL services means the customer may lose the Section 75 consumer protection, which means that refunds from faulty or non-received goods may not be possible through credit card payments. Therefore, banks need to offer more consumer protection in the longer term.

Jaimini Pattani, GlobalData banking analyst

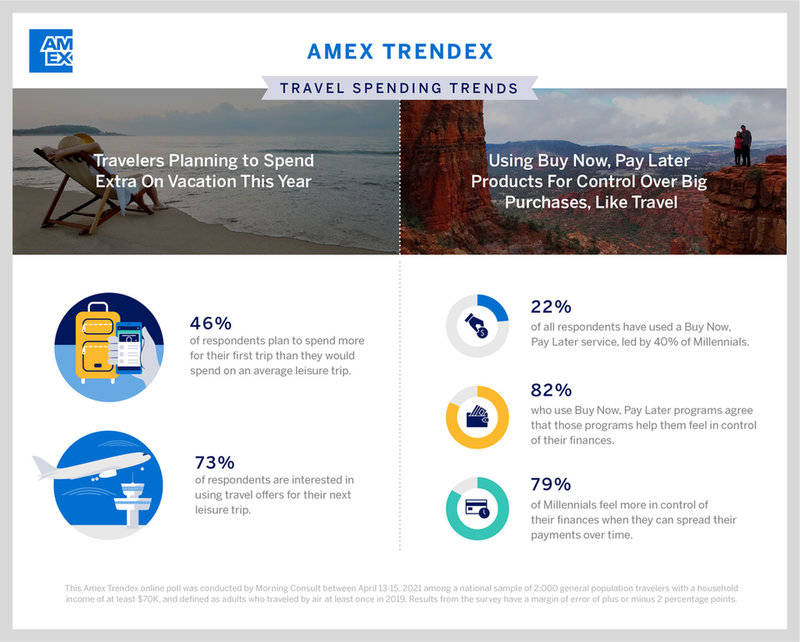

Travel Spending Trends factsheet. Source: AMEX