products

The Rise of cross-border financial services for migrants

UAE-based fintech Rise is bringing a raft of financial services to migrant workers. Rise acts as a financial hub, referring customers to partners that include Axa, Commercial Bank of Dubai and Carrefour UAE, writes Robin Arnfield

R

ise is already offering bank accounts, accident and disability insurance, and buy now pay later (BNPL) products. Its services are tailored to migrant workers who use its chatbot on their messaging apps to make financial plans, open a bank account, buy insurance and set up instalment payments.

An important innovation is that Rise provides migrants’ dependents back home with a tokenised version of the migrants’ payment cards that can be used online for limited purchases.

Rise was launched in 2017 by Padmini Gupta, Milind Singh and Mandeep Singh. Gupta, Rise’s CEO, has a background in banking and social change, while Milind Singh, chief product officer, has a background in strategy and fintech. Mandeep Singh, Rise’s chief technology officer, is a serial entrepreneur who has built several payment systems.

“We founded Rise with the simple idea of building a financial services platform that lets migrants manage their money across borders seamlessly,” Milind Singh tells EPI. “There are around 250 million migrants globally and a billion people worldwide depend on their remittances. Yet there is a lack of financial services products helping migrants manage this duality of living across borders.”

In March 2020, Rise raised a seven-digit investment in a funding round led by Middle East Venture Partners in partnership with Dubai International Financial Centre Fintech Fund, 500 Startups, Khwarizmi Ventures and Phoenician Funds. In March 2021, Rise raised additional funding from existing and new investors.

Milind Singh,

chief product officer, Rise

Accident and disability insurance from Axa

In the UAE, where 90% of the population are expatriates, Rise targets younger migrants with modest incomes of under AED5,000 ($1,361) a month who cannot get access to bank accounts, credit, insurance or investment advice.

Rise offers cross-border accident and disability insurance from Axa. According to Milind Singh, the French company had been wanting to provide a cross-border insurance product for migrants for some time, but, until partnering with Rise, had not found a way to make this possible.

Rise also offers UAE and cross-border BNPL loans. In the UAE, the service is offered at four Carrefour stores owned by Majid Al Futtaim. In Pakistan, Rise has partnered with e-commerce marketplace HomesShopping.pk to enable overseas Pakistanis to buy goods in Pakistan by making instalment payments in their country of residence.

“A Rise customer in the UAE can use our cross-border BNPL service to buy a TV for their family back home in instalments, which is a unique service,” says Milind Singh.

When it launched, Rise initially offered its customers prepaid cards and provided them with an app for managing their Rise accounts. “We were handling the customers’ funds in a prepaid account,” says Milind Singh.

“But we didn’t start Rise to be a bank account provider, as we’re interested in the cross-border piece. So, we stopped issuing prepaid cards and formed a partnership with Commercial Bank of Dubai, which offers fully fledged bank accounts with no minimum balance or salary requirements.”

This strategy is in contrast to UAE-based neobanks such as Now Money, which issue prepaid cards to low-income migrants.

Rise abandoned its app after it realised that its target customers didn’t have space on their phones for financial services apps, since they were full of social media and entertainment apps. “This meant we couldn’t get onto someone’s phone at the expense of WhatsApp or Facebook,” says Milind Singh.

Credit: Rise

Chatbot-based service since 2018

“So, in 2018 we moved to a completely chatbot-based service enabling customers to chat with us in their existing messaging app in their local language. So far, 500,000 people in the UAE have talked to us through our chatbot,” continues Milind Singh.

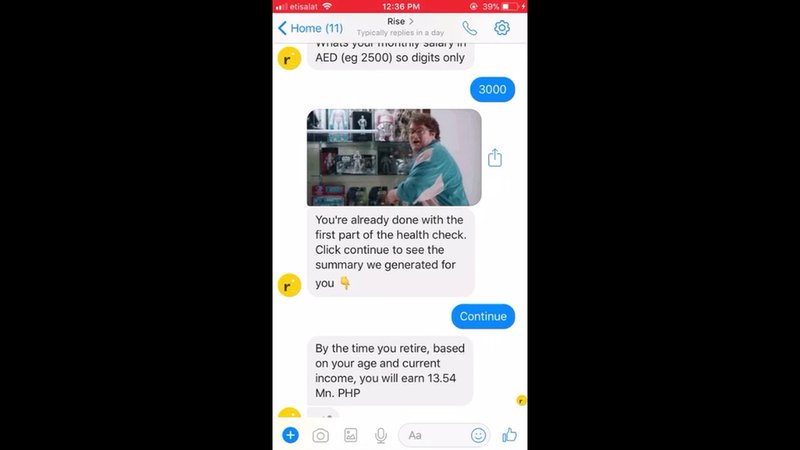

Customers can enquire about and apply for products using Rise’s chatbot and use its financial health check tool to calculate how much to save for their retirement. “We’re not investment advisers, so we have referral partnerships with investment firms in India and the Philippines for people who use our financial health check tool," Milind Singh explains.

According to Gupta, over 200,000 people have used Rise’s financial health check tool, which uses simple language to explain financial concepts. “Most banks’ financial health check tools require you to have an understanding of financial terminology, but our tool makes finance understandable,” she says.

Rise sees itself as the financial equivalent of Uber. “We don’t handle our customers’ assets or manage financial operations ourselves, as this would require us to comply with multiple regulations in different countries,” says Milind Singh.

“What we provide is a platform enabling consumers to access products from various financial services players. We generate revenues from referral fees from our partners.”

Padmini Gupta,

CEO, Rise

January 2021 launch of Xare

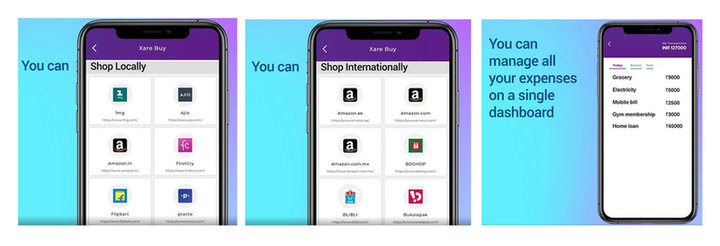

In January 2021, Rise launched Xare (pronounced ‘share’), an app targeting migrant workers globally who need to provide money for financial dependents while retaining oversight of beneficiaries’ spending. Unlike digital remittance apps such as Wise, Xare does not require beneficiaries to have bank accounts or e-money accounts.

“During the lockdown, migrants couldn’t send remittances home as cash, as money transfer agents’ offices were closed,” says Milind Singh. “We realised that migrants didn’t actually need to send money to their families back home. Instead, they could provide their relatives with access to their existing credit or debit cards without sending remittances.

“This means that Filipinos working in the UAE, for example, could enable their relatives back home to spend money from their UAE cards without needing to transfer funds to them.”

Xare gives the migrant who is the income-owner, visibility and control over where their money is being spent, as they can set daily or monthly limits, Milind Singh says. Also, their family back home has access to a payment instrument that they would not otherwise have access to, given the financial situation in their country.

“The context for Xare is that financial products are designed for people with an income,” says Milind Singh. “But only one-third of the world’s population have an income from work, and the remaining two-thirds spend someone else’s money. Yet, apart from Xare, there are no financial products that let the two-thirds have direct access to and spend the one-third’s money.”

To provide their dependents with access to their payment cards, Xare users simply select their phone number in their contact list.

“We have nearly 500,000 users of Xare in 115 countries. In South Asia, for example, we have tens of thousands of Xare users in every country. We have plans to offer a number of products through Xare.”

Xare users are not allowed to actually share their card account details with their beneficiaries. “We don’t provide beneficiaries with a virtual card, " explains Milind Singh. "Instead, we tokenise the migrant’s card details and enable the beneficiary to add this token to a digital payments app such as Google Pay. The maximum that the beneficiary can spend per month is $1,000 and they can only use the card for card-not-present purchases."