PRODUCTS

Canadian prepaid card sector posts 21% y-o-y growth

Jennifer Tramontana, co-founder and executive director at the Canadian Prepaid Providers Organisation (CPPO), tells Douglas Blakey that prepaid is driving innovation in the Canadian consumer banking ecosystem, and is the core offering with which most challenger banks launch in the market. Moreover, for the non-banks like tech giants, big retailers and e-commerce players, prepaid is the key to entry into the fintech space

T

he Canadian prepaid sector is in rude health according to the CPPO. Specifically, the prepaid industry in Canada has grown by 21% since 2020, with 38% of challenger banks offering prepaid cards. Kids and teen banking in particular is gaining traction, while real-time/early earnings access continues to grow in Canada and globally, by transferring payment to a prepaid card which can be used immediately.

Strong growth in Canada

Over the five-year period 2014-19, prepaid cards experienced the second-highest growth rate both in volume and value, the highest growth rate payment method being online transfers. The total volume of prepaid transactions totalled 328 million in 2019, growing 64% from five years prior. The total value of prepaid transactions totalled $19.2bn, growing 61.2% over the same period.

Canadians further developed their preference for utilising prepaid cards as their method of payment for e-commerce, with prepaid accounting for 10% of e-commerce transactions in 2019, significantly up from the 3% in 2018. Canadians were three times more likely to use a prepaid payment for e-commerce than they were at physical POS merchant locations.

Source: CPPO

Covid and its impact on prepaid

CPPO co-founder and executive director Jennifer Tramontana says the Covid pandemic has had a seismic impact on the Canadian financial ecosystem, and has shifted the way Canadians transact – which may be permanent in many ways.

She says: “Forty-four percent of Canadians say Covid-19 has changed their payments preferences to digital and contactless long-term, 61% are spending less, 42% are uncomfortable handling cash.”

Quoting research from Payments Canada, she adds that 32% of Canadians report using credit cards more, 21% report using debit cards more, and 25% report using e-transfer more.

Compared to pre-Covid use, 57% of Canadians report using cash less (compared to 65% in week five of the pandemic), 32% report using cheques less (down slightly from 35%), and 32% report using prepaid cards less (down from 37% in week five of the pandemic).

“Despite the decline in prepaid usage in 2020, which might trickle into 2021, prepaid offers opportunities for increasing financial inclusion and to play a key role in the post pandemic recovery,” Tramontana notes.

“Also, we are seeing more and more players launching or announcing plans to launch prepaid products in Canada, and thereby it is being predicted that prepaid usage will ramp up quickly over the next few years.”

Source: CPPO

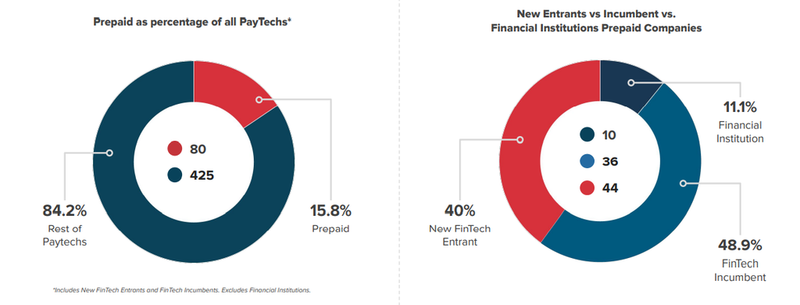

Of 34 challenger banks, 13 offer prepaid

“There are 34 challenger banks in Canada and 13 out of those have a prepaid card product – i.e. about 38% of the challenger banks in Canada offer prepaid cards. The vast majority of these prepaid enabled challenger banks are neobanks. In other words, they don't have a banking licence but they offer financial services through a banking partner who possesses a licence,” Tramontana continues.

There were 11 funding rounds in 2020-21, accounting for C$993m ($815m) invested in Canadian-headquartered prepaid ecosystem companies.

While most acquisitions by prepaid value chain players were related to acquiring for service provider or payment processing solutions, the most strategic prepaid related deals included the acquisition of Toronto-based challenger bank Stack by US-based fintech Credit Sesame, to launch Sesame Cash – a no-fee digital banking account.

Another notable deal was the acquisition of Montreal-based savings and investing app Moka by Vancouver-based challenger bank Mogo, to offer transaction round-up investing features on Mogo’s prepaid card and expand its wealth offering.

Kids' and teen banking gains traction

Tramontana is particularly upbeat about prepaid tapping into the growth in demand for kids and teen banking in Canada.

“These solutions allow parents to give money easily to their children," she explains. "They also enable them to track children's spending both online and in physical stores, set tasks that need to be completed for earning allowance, and help kids learn about savings.”

While most of these apps are meant for kids and teens to earn pocket money from their parents, a new player, SideKick, has emerged for international students in Canada. It enables them to receive money from their families in different currencies, and enables spending in Canada through a prepaid card. RBC Ventures has also launched Mydoh, a kids’ banking app backed by a prepaid card.

Source: CPPO

Real-time/early earnings access interest on the rise

Tramontana also flags up the growth in interest in real-time/early earnings access. Last year saw the rise of on-demand pay or earned wage access, and Canada has since seen many more players enter the space.

There is a variety of solutions ranging from anytime access during the pay cycle (Ceridian Dayforce), to two-day early access to payroll (PC Money), to same day earnings (Payfare), to access right after every shift (Payfare, Instant Financial).

The wage money is made accessible to the employee or gig worker by transferring it to a prepaid card which can be used immediately.

She concludes by arguing that prepaid players enable users to better budget, avoid overspending and get into the habit of savings by offering money management solutions. Challengers are also offering credit score monitoring and building solutions. These use-cases will further grow as open banking becomes live in Canada.

On that last point, given the UK experience to date, the jury is out. Also, for another day, is the often-vexed question of when a number of the prepaid sector players will move into profitability.

The report is, however, a must-read for anyone with an interest in Canadian consumer finance in general, and prepaid in particular.