Products & Services

The real-time payments revolution is underway

The mass adoption of real-time payment (RTP) systems around the globe has brought about a sea change in payments. Mohamed Dabo looks at a new report by ACI Worldwide and GlobalData

W

ith mobile technology and digital commerce driving the need for safer and faster payments, banks and businesses have seized upon real-time payments to create or enhance digital services for their customers.

The Covid-19 crisis has forced governments, businesses, and consumers to pay special attention to real-time payments.

Financial institutions of all sizes have joined the real-time payments revolution and a growing number of technology partners, funding agents, and core banking providers are working hard to provide RTP-related services.

More than 70.3 billion real-time payments transactions were processed globally in 2020.

This represents a surge of 41% compared to the previous year, as the Covid-19 pandemic dramatically accelerated trends away from cash and checks toward greater reliance on real-time and digital payments.

According to a new report by ACI Worldwide and GlobalData, the global boom in real-time payments is nothing short of a revolution.

Beating all expectations

Spurred by a year of unprecedented disruption, 2020 saw real-time payments grow larger—in terms of both volumes and values—and faster than anyone could have anticipated.

Changes to business models and consumer behaviour, prompted by the Covid-19 pandemic, have compressed many years’ worth of transformation and digitisation into the space of several months.

More people and more businesses around the world have access to real-time payments in more forms than ever before. Real-time Payments have been truly democratised, several years earlier than previously expected.

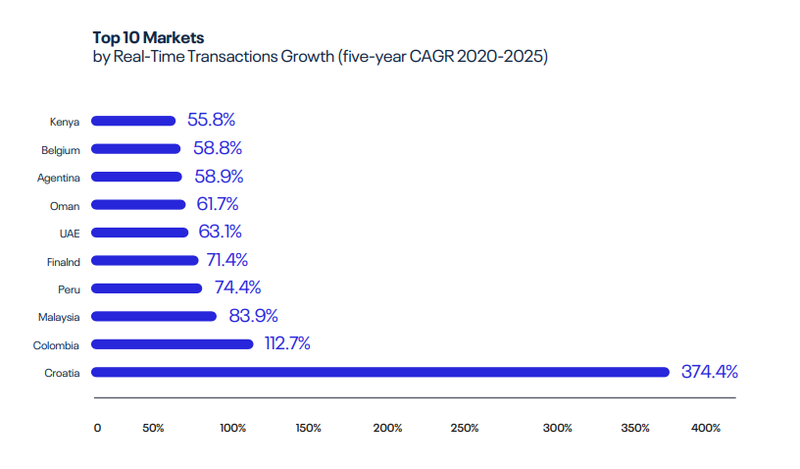

RTP Transaction. Credit: RTP

2020: the breakout year for real-time payments

As recently as two years ago, a national real-time payments infrastructure was considered a luxury in many markets.

That all changed in 2020, as the Covid-19 pandemic dramatically accelerated pre-existing but slow-moving trends away from cash and checks and towards greater reliance on digital payments in general, and real-time payments in particular.

Countries with robust digital payments infrastructure already in place have coped better than those without when it comes to containing the economic impact of the pandemic.

Real-time payments form a key part of that infrastructure, as they serve needs not supported by traditional card or ACH rails.

Real-time payments have enabled governments, working with their financial institutions, to accelerate much needed disbursements and economic stimulus payments to their citizens.

They have also enabled real-time liquidity to businesses that had to adapt to disrupted supply-and-demand patterns, including developing new supplier relationships with whom lines of credit had not yet been established.

The spotlight cast by the pandemic on existing payment infrastructures emphasised the systemic importance of digital payments.

Global volumes rose drastically, condensing a decade of anticipated innovation into one year and creating human behavioural changes that will not reverse as we emerge from the crisis.

RTP Growth. Credit: RTP

Changing the reality of payments

The accelerated adoption of mobile wallets, particularly in markets like the US, show that these kinds of unprecedented market events can alter cash and check trends even in the markets with the strongest grip.

Banks, processors, acquirers, and payment networks are under more pressure than ever to rapidly modernize their payment systems to manage this accelerated change.

At a national level, this means migrating to modern data standards, launching new real-time systems and new value-added services, such as Request to Pay.

And once the infrastructure is in place, the next imperative is for merchants to have more access to new payment services via the real-time rails.

This year’s research identified a new focus on digital payments acceptance and enabling real-time payments at the point of sale—both as the initial use case for a new system, such as PIX in Brazil, or as a modernization plan for existing realtime environments, such as the planned European Payments Initiative.

Markets that have a clear focus on the priority use cases for their consumers, merchants and financial institutions are among those experiencing the most rapid growth of real-time payment transactions.

What is clear from this year’s research and analysis is that the rate of change isn’t slowing.

Even in historically sluggish markets, 2020 was a catalytic year, resulting in new volumes, services and demands with which financial institutions must keep pace.

Managing this need for rapid innovation alongside serving the existing needs of customers calls for an agile approach to payments modernization.

We see success in this approach by regulators, networks, and financial institutions around the world.